Introduction

The duo of technology and automotive companies is heating up to a new level. For example, General Motors acquired Cruise Automation, a self-driving technology start-up company, in 2016 for a whopping sum of US$1 billion and announced that it would be collaborating with Lyft to test out self-driving taxis. Similarly, the electronic giant Sony announced a well-planned alliance with Honda Motors in March 2022 to create high-value battery-electric vehicles that will probably hit the roads by the year 2025. Moreover, smartphone behemoth Xiaomi also announced its entrance into the smart EV business in March of 2021.

Currently, an average car has about 90% hardware and about 10% software. However, as per industry reports, hardware’s share will come down to 40%, and the rest will be divided between software, which will be around 40%, and content, which will be approximately 20% in the future. Automotive experts believe that partnerships will be vital as it’s challenging for auto manufacturers to sustain their growth in the current disruptive era. Let’s discuss the roadmap for how the automotive industry might transition from 90% hardware to 40% hardware.

40% hardware for the future market of autonomous vehicles

Future business possibilities

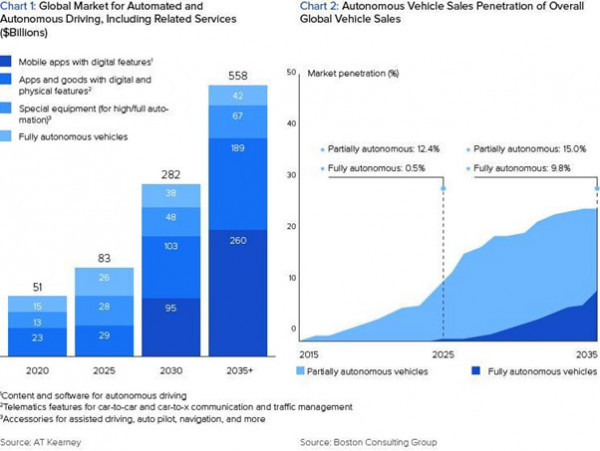

According to AT Kearney’s research, there are estimates that the market value of the connected mobility marketplace will leap to over US$550bn by the year 2035. Also, BCG provides an estimation that semi-autonomous or autonomous vehicle sales’ penetration could go to 25% by the same year.

A drastic shift in consumer behavior

As automotive technology advances further, a drastic shift in consumer behavior will transform the revenue model and value chain of the industry. Although the nature of these advances will be multifaceted, we can categorize them into two main buckets at a high level.

Time spent in vehicles

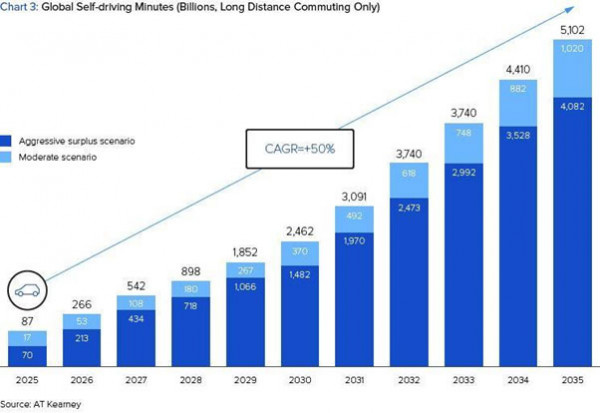

The first significant change related to the automotive industry is the time spent in vehicles on driving. Of course, people already spend a lot of time in their cars: According to AAA Foundation estimations, US drivers spend more than 290 hours every year driving around, which equates to approximately 6-7 hours per licensed driver per week. But with the introduction of autonomous vehicles, the number is likely to reduce significantly over time. The logic is simple: as cars transform into self-driving vehicles with 40% hardware, people will have more time to perform other tasks while traveling. According to AT Kearney’s estimation, self-driving technology can offer up to 1.9 trillion minutes of free time for passengers by the end of 2030.

Global self-driving minutes estimation

Growth of mobility-as-a-service

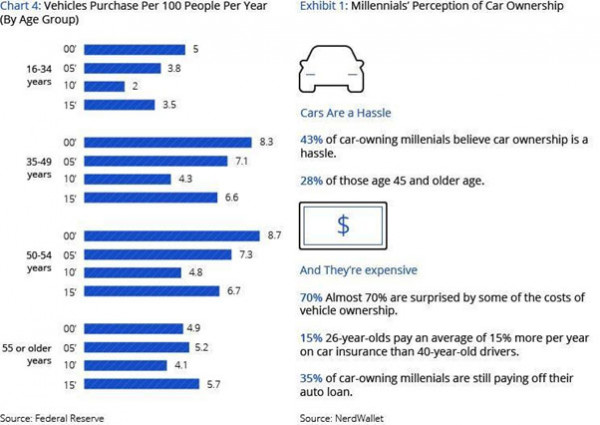

The other fundamental change in consumer behavior due to autonomous vehicles is the growth of mobility-as-a-service. It refers to a shift from personally-owned vehicles to using mobility solutions on-demand. Over the years, car ownership has moved from a status symbol to a utility-driven one. Self-driven vehicles will accelerate this trend further.

Changing trends in car ownership

A new value chain

The transition from 90% hardware to 40% hardware

We are probably going to see the automotive industry evolve from an OEM-led value chain toward a “technology stack” that in numerous ways mimics what we have seen happening in the computer industry. The automotive industry will be divided into three categories.

- Hardware Companies: Producing physical components of the vehicles

- Software Companies: Providing intelligence to run vehicles and also building connectivity and fleet management functionality

- Applications: This will leverage both hardware and software to offer customers the best service and experience

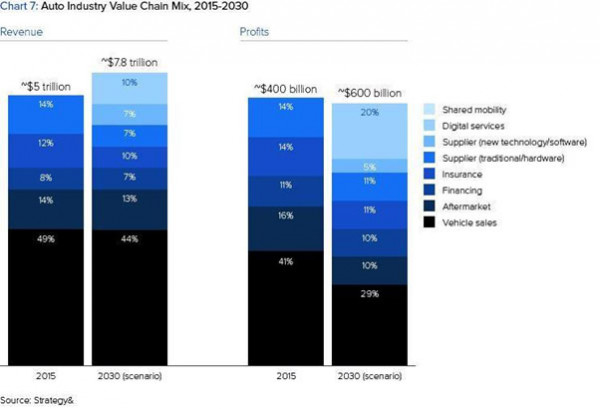

According to Morgan Stanley’s estimation, the software and application layers in combination will account for 60% of the value chain, and the rest will be the hardware supply, significantly reduced from 90% to 40%. Hence, hardware suppliers must adapt to this challenge and evolve accordingly. As per strategy and estimation, the revenue share of hardware companies will deteriorate, and their share of industry profits will decline even more substantially.

Automotive industry value chain 2015-2030 trend

How to turn around the future

As there is a big chance of long-term decline with respect to hardware revenue share, the OEMs will try to enter the software and applications layer and continue to stay relevant in the era of self-driving vehicles. Here are a few considerations.

- Work in partnership with all technology companies developing OS solutions to make sure that the hardware or software integration is done as smoothly as possible.

- Go for both hardware optimization and application development simultaneously.

- Choose the right talent to make the transition from 90% hardware to 40% hardware in a smooth way.

Conclusion

The transition from 90% hardware to 40% hardware in the automotive industry will happen somewhere down the line; hence, all involved parties must be ready to embrace it and look for strategies to sustain their growth.